|

The two big issues for the U.S. economy are job growth and resolution of sovereign debt problems in Europe. There was progress on both issues this past week though there was uncertainty early in the week.

Equities dropped sharply early in the week on overseas worries but made a sizeable comeback the last three days on progress on Greek debt and on a better-than-expected jobs report. Equities dropped sharply early in the week on overseas worries but made a sizeable comeback the last three days on progress on Greek debt and on a better-than-expected jobs report.

At the start of the week, the main “problem” was China, not Greece, after China cut its growth target for 2012 to 7.5 percent from 8.0 percent. Equities declined despite countervailing news that the ISM non-manufacturing index rose to its highest level in a year. Weighing on stocks were reports from Greece that it would enforce losses on private creditors, indicating that not enough creditors were signing up for its debt-swap offer. Thursday was the deadline for reaching agreement on the debt-swap offer (old bonds heavily discounted for new bonds).

Tuesday, data showing fourth quarter contraction in Europe’s economy bumped stocks down with growing concern that there would not be voluntary settlement in the Greek debt-swap offer. Tuesday posted the largest decline of 2012 for many indexes, including the Dow and S&P 500.

At mid-week, an unexpectedly strong gain in ADP private employment boosted stocks. Optimism about Greece’s debt swap also lifted stocks as it appeared that private creditors—despite last minute games of “chicken”—were signing up for the debt swap. Also lifting stocks were rumors that the Fed is considering “sterilized” quantitative easing as an additional easing measure. Allegedly, the Fed would buy long-term bonds while offsetting the purchases with sales of assets elsewhere.

Stocks posted another strong day Thursday as Greece appeared to be on track to secure a deal with bondholders as part of a financial bailout. Greece was reported to have had more private creditors sign up for the swap arrangement than the minimum needed. At week’s close, a strong-than-expected payroll employment increase for February and upward revisions to the prior two months boosted stocks notably even though Greece finally officially defaulted. But now it will be an orderly default with a swap agreement being put into place.

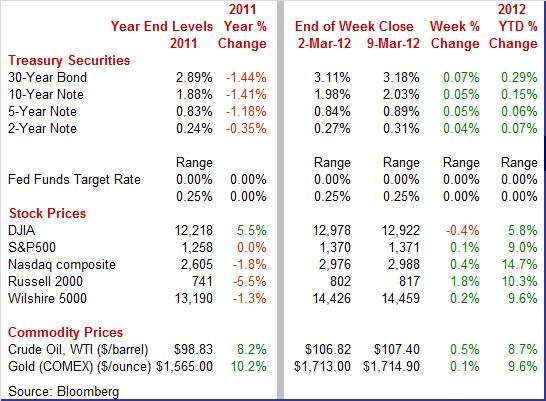

By close for the week, most major indexes were up for the week but with the Dow being an exception.

Equities were mostly up this past week. The S&P 500 was up 0.1 percent; the Nasdaq, up 0.4 percent; and the Russell 2000, up 1.8 percent. The Dow dipped 0.4 percent.

For the year-to-date, major indexes are up as follows: the Dow, up 5.8 percent; the S&P 500, up 9.0 percent; the Nasdaq, up 14.7 percent; and the Russell 2000, up 10.3 percent.

Weekly percent change column reflects percent changes for all components except interest rates. Interest rate changes are reflected in simple differences.

Treasury yields rose moderately net for the past week. At the start of the week, bond traders had a different focus than equity traders, placing greater emphasis on the boost in the ISM non-manufacturing index and lifting rates somewhat. Treasury yields rose moderately net for the past week. At the start of the week, bond traders had a different focus than equity traders, placing greater emphasis on the boost in the ISM non-manufacturing index and lifting rates somewhat.

But for the rest of the week, yields tracked movement in stocks. Rates dipped Tuesday on flight to safety from European economic contraction and lack of progress on Greek debt.

Mid-week saw a firming in rates on the ADP report and growing expectations that a Greek settlement would be reached, reversing flight to safety. The increasing likelihood of a swap arrangement for Greece lifted rates Thursday. The healthy jobs report nudged up Treasury yields at week’s close as Greece’s official default on the day was expected and now orderly. Mid-week saw a firming in rates on the ADP report and growing expectations that a Greek settlement would be reached, reversing flight to safety. The increasing likelihood of a swap arrangement for Greece lifted rates Thursday. The healthy jobs report nudged up Treasury yields at week’s close as Greece’s official default on the day was expected and now orderly.

For this past week Treasury rates were up as follows: 3-month T-bill, up 2 basis points; the 2-year note, up 4 basis points; the 5-year note, up 5 basis points; the 7-year note, up 4 basis points; the 10-year note, up 5 basis points; and the 30-year bond, up 7 basis points.

Crude oil prices firmed marginally but were essentially unchanged this past week. The biggest swings were Tuesday and Wednesday. After a quiet Monday, the spot price of West Texas Intermediate on Tuesday jumped two dollars a barrel after the European Union offered to restart negotiations with Iran over its nuclear program, reducing the risk of war in the region. Also, a report showed economic contraction in the euro zone for the fourth quarter. Crude oil prices firmed marginally but were essentially unchanged this past week. The biggest swings were Tuesday and Wednesday. After a quiet Monday, the spot price of West Texas Intermediate on Tuesday jumped two dollars a barrel after the European Union offered to restart negotiations with Iran over its nuclear program, reducing the risk of war in the region. Also, a report showed economic contraction in the euro zone for the fourth quarter.

Optimism about progress on Greek debt boosted crude by a buck and a half at midweek with the healthy ADP employment report also contributing. Friday’s favorable employment report boosted crude somewhat less than a dollar a barrel.

Net for the week, the spot price for West Texas Intermediate nudged up 58 cents per barrel to settle at $107.40. The price of crude remains notably elevated relative to latter 2011.

Economic news was largely favorable, indicating that the recovery is slowly gaining traction. The latest employment report was encouraging.

Employment gains continued at a moderately healthy pace in February while the unemployment rate was unchanged 8.3 percent. Upward revisions to payrolls were notable. Payroll jobs in February grew 227,000 after gaining 284,000 in January (originally 243,000) and rising 223,000 in December (prior estimate up 203,000). The net revisions for December and January were up 61,000. Overall payroll jobs now have risen more than 200,000 for three months in a row. Employment gains continued at a moderately healthy pace in February while the unemployment rate was unchanged 8.3 percent. Upward revisions to payrolls were notable. Payroll jobs in February grew 227,000 after gaining 284,000 in January (originally 243,000) and rising 223,000 in December (prior estimate up 203,000). The net revisions for December and January were up 61,000. Overall payroll jobs now have risen more than 200,000 for three months in a row.

Private payrolls were slightly stronger than overall, rising 233,000 in February after a 285,000 boost the month before. Analysts expected a 220,000 advance. Private-sector employment was led by services-providing industries with a 209,000 boost, following a 202,000 increase in January. By industry, job gains were strongest in professional and business services, health care and social assistance, and leisure and hospitality. Private payrolls were slightly stronger than overall, rising 233,000 in February after a 285,000 boost the month before. Analysts expected a 220,000 advance. Private-sector employment was led by services-providing industries with a 209,000 boost, following a 202,000 increase in January. By industry, job gains were strongest in professional and business services, health care and social assistance, and leisure and hospitality.

In goods-producing industries, manufacturing and mining also posted notable gains while construction employment slipped. Manufacturing gained 32,000 after a 52,000 jump in January. Mining rose 7,000 after a 10,000 gain. However, construction jobs fell back 13,000 after a 21,000 boost the month before.

The public sector continued to shrink but at a more modest pace than in recent months as government employment eased 6,000, following a 1,000 slip in January.

Average hourly earnings rose a modest 0.1 percent in February, following a 0.1 percent gain the month before. The market median forecast was for a 0.2 percent improvement. The average work week for all workers in February was unchanged at 34.5 hours. Expectations were for 34.5 hours.

There were more positive than negative signs of forward momentum from the establishment survey. On the negative side, retail employment slipped 7,000 but followed a strong 26,000 boost in January. Hiring of temp help jumped 45,000 in February, following a 32,000 increase the month before. Businesses often boost temp hires before permanent hires. The temp help gain in February was the largest since January 2010. Lastly, there are signs that consumers are feeling good enough about job security and income to boost discretionary spending. Hiring by restaurants and bars jumped 41,000 in February after a 31,000 gain in January.

From the household survey, the steady unemployment rate reflected gains in both household employment and the labor force. Analysts had forecast an 8.3 percent unemployment rate. The labor force jumped 476,000 in the latest month but household jobs closely followed, rising 428,000. Among the unemployed, the number of job leavers rose by 92,000, indicating that the job market is improving. Workers normally do not voluntarily quit a job unless they have another one waiting.

Looking ahead, there are positive signs for personal income and industrial production. The private wages & salaries component in personal income is likely to post a healthy gain in February as aggregate private earnings rose 0.4 percent. The manufacturing component of industrial production also should post a notable gain as production worker hours in manufacturing advanced 0.6 percent. The healthy manufacturing numbers are favorable for first quarter GDP although mild weather likely has damped utilities output.

Overall, the latest report shows the labor market gradually improving and providing modest momentum to the consumer sector. Still, growth is not strong enough to make much of a dent in unemployment.

Consumers are definitely borrowing again based on a major five-month surge in outstanding credit, the latest a $17.8 billion gain in January versus a revised $16.3 billion gain in December. During the five months, outstanding credit has jumped $68.5 billion. At $2.512 trillion, total outstanding credit is only $70 billion below its July 2008 peak of $2.582 trillion. Consumers are definitely borrowing again based on a major five-month surge in outstanding credit, the latest a $17.8 billion gain in January versus a revised $16.3 billion gain in December. During the five months, outstanding credit has jumped $68.5 billion. At $2.512 trillion, total outstanding credit is only $70 billion below its July 2008 peak of $2.582 trillion.

In what is nearly a new record for an old series, non-revolving credit, surged $20.7 billion in the month after increasing $12.6 billion in December. The big gain for the latest month offset a slight decline in revolving credit which nevertheless, reflecting increasing use of credit cards, continues to trend higher.

While much of the recent gains in non-revolving credit has been due to strength in auto sales, there also has been an uptrend in student loans. The Fed does not seasonally adjust components within non-revolving credit and NSA student loan debt through Sallie Mae jumped $27.1 billion. Of course, student loans typically spike in January at the start of the year and semester. While much of the recent gains in non-revolving credit has been due to strength in auto sales, there also has been an uptrend in student loans. The Fed does not seasonally adjust components within non-revolving credit and NSA student loan debt through Sallie Mae jumped $27.1 billion. Of course, student loans typically spike in January at the start of the year and semester.

Econoday ran the Sallie Mae numbers through seasonal adjustment software (Census X-11) and came up with a seasonally adjusted increase of $10.1 billion after a $17.1 billion jump in December. This means that for the latest month, strength in non-revolving credit was about evenly divided between student loans and auto loans. Student loans are up due to increased availability of funds from Sallie Mae and also due to a weak job market meaning more students remaining in school.

Higher oil prices led to more red ink for the U.S. trade gap for the latest month. The U.S. trade deficit expanded in January to $52.6 billion from $50.4 billion in December (originally $48.8 billion). Exports advanced 1.4 percent after rebounding 0.4 percent in December. But imports grew a sharp 2.1 percent in January, following a 1.6 percent increase the prior month. Higher oil prices led to more red ink for the U.S. trade gap for the latest month. The U.S. trade deficit expanded in January to $52.6 billion from $50.4 billion in December (originally $48.8 billion). Exports advanced 1.4 percent after rebounding 0.4 percent in December. But imports grew a sharp 2.1 percent in January, following a 1.6 percent increase the prior month.

The worsening in the trade gap was led by the petroleum goods deficit which widened to $29.7 billion from $27.2 billion in December. The nonpetroleum goods gap, however, was little changed at $36.8 billion from $36.7 billion the month before. The services surplus improved to $14.9 billion from $14.6 billion. Services exports hit an all-time high at $52.2 billion for the month.

Goods exports were led by capital goods excluding autos and autos. Goods imports were led by autos and by industrial supplies.

Excluding petroleum, goods exports jumped 2.3 percent in January after rising 0.4 percent the month before. Excluding petroleum, goods imports were up 1.8 percent after a 2.1 percent gain.

The chain-dollar trade gap worsened to $49.1 billion from $48.3 billion in December, suggesting that economists may nudge down their estimate for net exports in first quarter GDP.

The widening of the deficit was mostly (but not entirely) expected due to higher oil prices. This is a negative for the consumer’s wallet. But the good news within the report is that nonpetroleum goods exports are still healthy—making manufacturers happy and providing support for continued economic growth.

There are further indications that the recovery is improving beyond manufacturing. The ISM non-manufacturing composite index for February rose five tenths to 57.3—the highest level since February 2011 and well over breakeven of 50 to indicate moderately strong growth. There are further indications that the recovery is improving beyond manufacturing. The ISM non-manufacturing composite index for February rose five tenths to 57.3—the highest level since February 2011 and well over breakeven of 50 to indicate moderately strong growth.

Rising orders stood out as the new orders index gained 1.8 points in February to a robust 61.2. Strength in new orders is feeding a build in backlog orders which rose 3.5 points to 53.0 which is a strong level for this reading.

Other activity is tracking orders with business activity (akin to a production index) up more than three points to a very strong 62.6. Another key reading shows moderating strength in employment to a still very strong 55.7.

Overall, the report confirms growing strength for the economy, indicating that momentum is slowing spreading beyond manufacturing.

It is still very gradual but the recovery is improving as suggested by the latest reports on employment and non-manufacturing. And detail within international trade indicates that export growth is still at a healthy pace.

The highlights for the week are on Tuesday with the consumer update from retail sales and the Fed’s meeting statement pointing to new easing or not. Inflation news posts Thursday and Friday with the PPI and CPI. Manufacturing updates hit the wires with Empire State and Philly Fed on Thursday and industrial production to close the week.

The U.S. Treasury monthly budget report showed a January deficit totaling only $27.4 billion, roughly half the Econoday consensus for $50.1 billion. Much of the improvement was due to timing issues for benefits which were moved into December. Fundamentally though, much of the improvement reflected a 3 percent year-on-year increase in receipts. Looking ahead, the month of February typically shows a deficit for the month. Over the past 10 years, the average deficit for the month of February has been $126.1 billion and $165.9 billion over the past 5 years. The February 2011 deficit came in at $222.5 billion.

Treasury Statement Consensus Forecast for February 12: -$229.0 billion

Range: -$229.4 billion to -$25.0 billion.

The NFIB Small Business Optimism Index in January rose one tenth to 93.9. More expect the economy to improve and more job openings were reported, but earnings trends are down as is sentiment on inventories which the NFIB panel expects to further reduce. While the index is up for a fifth straight month, the report points to a slow and weak pace for economic growth.

NFIB Small Business Optimism Index Consensus Forecast for February 12: 95.0

Range: 94.0 to 95.2

Retail sales in January jumped 0.4 percent after no change the month before. Restraining the gain was weakness in the auto component which dropped 1.1 percent, following a 2.5 percent jump in December. Excluding autos, retail sales surged 0.7 percent in January after decreasing 0.5 percent in December. Gasoline sales increased 1.4 percent after a 2.6 percent drop in December. Sales excluding autos and gasoline in January rebounded 0.6 percent, following a 0.2 percent dip the prior month. Gains were broad based. More recently, unit new motor vehicle sales in February surged a monthly 6.5 percent, suggesting a strong gain in the auto component of retail sales.

Retail sales Consensus Forecast for February 12: +1.2 percent

Range: +0.7 to +2.1 percent

Retail sales excluding motor vehicles Consensus Forecast for February 12: +0.8 percent

Range: +0.4 to +1.7 percent

Less motor vehicles & gasoline Consensus Forecast for February 12: +0.6 percent

Range: +0.3 to +0.9 percent

Business inventories rose a moderate 0.4 percent in December, below the 0.7 percent rise for sales and pulling down the stock-to-sales ratio by 1 tenth to 1.26. More recently, for January manufacturers’ inventories gained 0.6 percent while wholesaler inventories advanced 0.4 percent.

Business inventories Consensus Forecast for January 11: +0.5 percent

Range: +0.3 to +0.6 percent

The FOMC announcement at 2:15 p.m. ET for the March 13 FOMC policy meeting is expected to leave rates unchanged. Market focus will be on comments on changes in the relative strength of the economy, changes in inflation worries, and whether the Fed is willing to undertake new options. Market expectations likely were raised by the March 7 Wall Street Journal article (unnamed sources) stating that the Fed is considering “sterilized” buying of long-term bonds—shifting the average maturity of the Fed’s holdings and offsetting the longer-term purchases with sales elsewhere on the balance sheet. But several District presidents oppose QE3 and likely will raise questions about this new idea. Key questions likely would be whether the Fed will lose money on these transactions as interest rates rise. And if the Fed will lose money, will that impede how quickly the Fed can unwind its balance sheet as the economy eventually heats up. And even will potential Fed losses have an impact on the federal deficit (annual Fed profits are handed over to the Treasury). The cost/benefit analysis for the alleged new Fed option may not play out well.

FOMC Consensus Forecast for 3/13/12 policy vote on fed funds target range: unchanged at a range of zero to 0.25 percent

Import prices rose 0.3 percent rise in January. But excluding a sizable 1.2 percent monthly jump in petroleum prices, import prices were unchanged and remained tame. Export prices rose 0.2 percent in January with a 1.1 percent monthly gain in agricultural prices offset by wide declines in other components.

Import prices Consensus Forecast for February 12: +0.6 percent

Range: +0.2 to +1.7 percent

Export prices Consensus Forecast for February 12: +0.3 percent

Range: +0.2 to +0.4 percent

Initial jobless claims in the March 3 week rose 8,000 to 362,000 with the prior week revised 3,000 higher. There were no special factors distorting the data. The February 11 week is the recovery low so far for claims at 351,000. A long streak of improvement in the four-week average was snapped at seven weeks with the average up, but only fractionally, to 355,000.

Jobless Claims Consensus Forecast for 3/10/12: 355,000

Range: 350,000 to 372,000

The producer price index rebounded 0.1 percent in January, following a 0.1 percent dip the prior month. The core PPI jumped 0.4 percent, following a 0.3 percent rise in December. By major components, energy declined 0.5 percent in January, following a 0.4 percent decrease. Food decreased 0.3 percent in the latest month. Upward pressure in the core came from pharmaceuticals, light trucks, and tobacco products.

PPI Consensus Forecast for February 12: +0.5 percent

Range: +0.3 to +0.7 percent

PPI ex food & energy Consensus Forecast for February 12: +0.2 percent

Range: 0.0 to +0.3 percent

The Empire State manufacturing index for February rose 6.05 points to 19.53 for the best reading in more than a year and a half. But details showed less strength with new orders down 4 points to 9.73, a level that's comfortably above zero to indicate a month-to-month increase in orders but still lower than January to indicate a monthly slowing in the rate of increase.

Empire State Manufacturing Survey Consensus Forecast for March 12: 17.50

Range: 12.00 to 24.70

The general business conditions index of the Philadelphia Fed's Business Outlook Survey in February rose 2.9 points to 10.2, indicating healthy activity in the Mid-Atlantic manufacturing sector. But readings on expectations pointed to possible slowing ahead with the Philly's 6-month outlook taking a particularly steep dive of nearly 16 points. But most details in the Philly report were positive including acceleration for new orders, a build in backlog orders, acceleration in shipments, and a draw in inventories that points to the need for replenishment.

Philadelphia Fed survey Consensus Forecast for March 12: 11.5

Range: 6.7 to 16.0

Quadruple Witching

The consumer price index in January rose 0.2 percent, following no change in each of the prior two months. Excluding food and energy, the CPI firmed to a 0.2 percent increase from December’s 0.1 percent increase. Energy rose only 0.2 percent, following a 1.3 percent decrease in December. Food price inflation held steady at 0.2 percent. Within the core, upward pressure came from apparel, recreation, tobacco, and medical care. In contrast to these increases, the index for used cars and trucks declined for the fifth month in a row and the index for airline fares dipped in the latest month.

CPI Consensus Forecast for February 12: +0.5 percent

Range: +0.3 to +0.6 percent

CPI ex food & energy Consensus Forecast for February 12: +0.2 percent

Range: +0.1 to +0.2 percent

Industrial production overall was unchanged in January after a 1.0 percent jump the month before. By major components, manufacturing jumped 0.7 percent, following a 1.5 percent comeback in December. In January, utilities dropped 2.5 percent while mining output declined 1.8 percent. More recently, aggregate production worker hours in manufacturing for February posted a healthy 0.6 percent boost, indicating a robust increase for the manufacturing component of industrial production.

Industrial production Consensus Forecast for February 12: +0.5 percent

Range: +0.2 to +1.0 percent

Manufacturing production component Consensus Forecast for February 12: +0.5 percent

Range: +0.4 to +0.6 percent

Capacity utilization Consensus Forecast for February 12: 78.8 percent

Range: 78.5 to 79.0 percent

The Reuters/University of Michigan's consumer sentiment index rose three tenths from January for a final February reading 75.3. This compared to mid-February at 72.5 and reflected a strong second-half showing with the implied reading for the period at 78.1 in what would be the best level of the recovery so far.

Consumer sentiment index Consensus Forecast for preliminary March 12: 76.0

Range: 73.0 to 78.8

R. Mark Rogers is the author of The Complete Idiot’s Guide to Economic Indicators, Penguin Books, 2009.

Econoday Senior Writer Mark Pender contributed to this article.

|