|

Job growth finally made its long-awaited comeback in the latest employment situation report. And manufacturing is showing further strengthening. But high oil prices are casting a shadow over economic growth while housing remains anemic.

Most major indexes ended the week up incrementally despite sharp daily volatility. And the favorable jobs report was not enough to prevent a sell off at the week's close. Equities likely would be more positive if not for the downdraft from rising oil prices. Most major indexes ended the week up incrementally despite sharp daily volatility. And the favorable jobs report was not enough to prevent a sell off at the week's close. Equities likely would be more positive if not for the downdraft from rising oil prices.

The week got off to a moderately positive start as a strong-than-expected Chicago PMI more than offset a dip in pending home sales. Comments by billionaire investor Warren Buffet that he was in a mood for buying companies put the bulls in a good mood, helping to lift stocks. But Tuesday was a notably down day with major indexes down from about 1.5 percent to over 2 percent. A more than two and a half buck surge in oil prices to just under $100 per barrel for WTI spot (just over $100 for futures) was the major culprit.

Equities fought back at mid-week as favorable economic news offset another boost in oil prices. The ADP employment report posted a sizeable gain in private employment and the Fed’s Beige Book noted improvement in all 12 Districts and momentum building in the manufacturing and consumer sectors. The biggest boost for equities was Thursday as initial jobless claims fell sharply instead of posting a modest rise as forecast. Also, the Bloomberg Consumer Comfort Index showed consumers increasingly saying their finances are in good shape. Finally, a better-than-expected rise in the ISM non-manufacturing index added to upward momentum. Thursday’s news boosted expectations for the next day’s jobs report.

Equities were down notably the last trading day of the week with several factors coming into play. First, the February employment situation report was initially seen as close to expectations and there was little immediate reaction. However, upon quick re-evaluation, the overall payroll gain of 192,000 was seen falling short of whisper upgrades to market forecasts (following an unexpected drop in jobless claims on Thursday) that called for notably higher than the printed 200,000 forecast. Second, the flat number for average hourly earnings got more attention as the day wore on and oil prices rose. Consumer wages were seen as falling further and further behind inflation with the flat reading on wages. So, the boost in oil prices probably was the biggest factor behind stock market losses for the day. Separately, some traders took the view that the moderately healthy gain in payroll jobs will lead the Fed to raise rates by the end of the year. But at Friday’s close, equities were up modestly for the week.

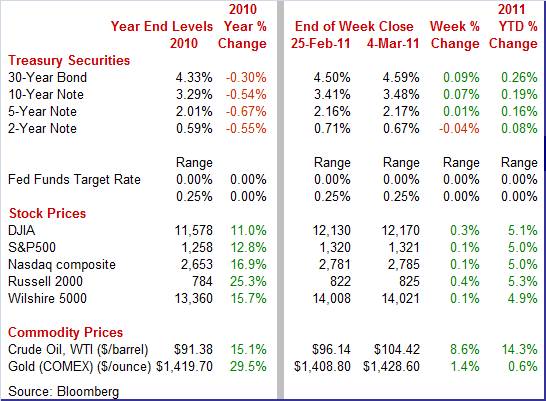

Equities were up this past week. The Dow was up 0.3 percent; the S&P 500, up 0.1 percent; the Nasdaq, up 0.1 percent; and the Russell 2000, up 0.4 percent. Equities were up this past week. The Dow was up 0.3 percent; the S&P 500, up 0.1 percent; the Nasdaq, up 0.1 percent; and the Russell 2000, up 0.4 percent.

Equities were up for February. The Dow was up 2.8 percent; the S&P 500, up 3.2 percent; the Nasdaq, up 3.0 percent; and the Russell 2000, up 5.4 percent.

For the year-to-date, major indexes are up as follows: the Dow, up 5.1 percent; the S&P 500, up 5.0 percent; the Nasdaq, up 5.0 percent; and the Russell 2000, up 5.3 percent.

Weekly percent change column reflects percent changes for all components except interest rates. Interest rate changes are reflected in simple differences.

The big moves this past week for Treasuries were on Wednesday, Thursday, and Friday. The big moves this past week for Treasuries were on Wednesday, Thursday, and Friday.

Rates bumped up at mid-week on a strong ADP employment report, projecting that private employment jobs for February would come in at 217,000 and on the Fed’s Beige Book indicating a strengthening in the recovery. Thursday saw yields rise further on the drop in jobless claims and ISM non-manufacturing number.

Rates retreated Friday almost entirely on flight to safety. A notable drop in equities on disappointment over the jobs report led funds to flow into Treasuries. Also, increased turmoil in the Middle East and North Africa added to flight. Rates retreated Friday almost entirely on flight to safety. A notable drop in equities on disappointment over the jobs report led funds to flow into Treasuries. Also, increased turmoil in the Middle East and North Africa added to flight.

For this past week Treasury rates were mostly up as follows: the 5-year note, up 1 basis point; the 7-year note, up 5 basis points; the 10-year note, up 7 basis points; and the 30-year bond, up 9 basis points. The 3-month T-bill slipped 1 basis point while the 2-year note dipped 4 basis points.

Treasury yields appear to still be on a gradual uptrend on a stronger economy (raising the demand for loanable funds), higher inflation worries, and concern over a still lofty federal deficit. Of course, the short end remains pinned down by a near-zero fed funds target rate.

The price of crude marched strongly and almost steadily upward all week with a slight pause only on Thursday. Gains of over $2-1/2 per barrel were seen on Tuesday, Wednesday, and Friday. The price of crude marched strongly and almost steadily upward all week with a slight pause only on Thursday. Gains of over $2-1/2 per barrel were seen on Tuesday, Wednesday, and Friday.

A strong ISM manufacturing report boosted crude Tuesday along with reports that Iranians authorities arrested opposition leaders in order to hinder scheduled demonstrations. At midweek-news that forces loyal to Libyan strongman Muammar Qaddafi attacked rebel positions on the east coast where most of the country’s oil refineries and shipping points are bumped up the spot price for West Texas Intermediate. Prices were lifted to a 29-month high on worries that unrest in Libya might spread to key oil exporters in the Middle East—including Saudi Arabia.

Net for the week, spot prices for West Texas Intermediate surged $8.28 per barrel to settle at $104.42—the highest settle since September 2008.

Economic news this past week was largely positive. Employment finally looks respectable again and manufacturing is gaining strength. However, the single-family component of housing appears to be losing some ground.

The latest payroll numbers in the employment report provided welcome relief from very sluggish gains in recent months. Overall payroll employment in February grew by 192,000, following a revised 63,000 rise in January and a 152,000 gain in December. The February advance came in marginally lower than the updated consensus forecast for a 200,000 gain. The December and January revisions were up net 58,000. Private nonfarm payrolls were somewhat stronger, increasing 222,000 in February, following a 68,000 boost in January. Analysts had projected a 190,000 advance in the latest month. The latest payroll numbers in the employment report provided welcome relief from very sluggish gains in recent months. Overall payroll employment in February grew by 192,000, following a revised 63,000 rise in January and a 152,000 gain in December. The February advance came in marginally lower than the updated consensus forecast for a 200,000 gain. The December and January revisions were up net 58,000. Private nonfarm payrolls were somewhat stronger, increasing 222,000 in February, following a 68,000 boost in January. Analysts had projected a 190,000 advance in the latest month.

By major sectors, the goods-producing numbers look good, showing a 70,000 jump, following a 35,000 rise in January. For the latest month, manufacturing jobs advanced 33,000 after a 53,000 boost in January. Even better, only 1,000 of the February gain in manufacturing was for motor vehicles. Construction employment increased 33,000 in February, following a 22,000 decline the prior month. Mining rose 4,000 in February.

Private service-providing jobs jumped 152,000 after a 33,000 increase in January. The latest was led by a gain of 47,000 in professional and business services with 16,000 coming from temp help. Government jobs fell 30,000, following a 5,000 dip in January. Private service-providing jobs jumped 152,000 after a 33,000 increase in January. The latest was led by a gain of 47,000 in professional and business services with 16,000 coming from temp help. Government jobs fell 30,000, following a 5,000 dip in January.

A disappointment in the employment report was in earnings. Wage pressures eased in February as average hourly earnings were flat in February, following a 0.4 percent jump the previous month. However, given that February followed a very strong January, the latest number is not so worrisome.

On a year-ago basis, earnings growth is soft—up 2.1 percent in February compared to up 2.2 percent the prior month.

Turning to the household survey, the unemployment rate edged down to 8.9 percent from 9.0 percent in January. Analysts had expected 9.1 percent. What was behind the decline' For February, household employment increased 250,000 while the number of unemployed dropped 190,000. Most of the decrease in unemployment was for those unemployed 15 weeks or more. This suggests an increase in discouraged workers dropping out of the workforce.

What forward looking information is there for economic news later this month' First, aggregate earnings for all employees rose a modest 0.2 percent. This suggests that the wages & salaries component in February personal income is going to be posting only a modest increase. However, production worker hours in manufacturing jumped a strong 0.6 percent, indicating that the manufacturing component of industrial production should be robust for the month. What forward looking information is there for economic news later this month' First, aggregate earnings for all employees rose a modest 0.2 percent. This suggests that the wages & salaries component in February personal income is going to be posting only a modest increase. However, production worker hours in manufacturing jumped a strong 0.6 percent, indicating that the manufacturing component of industrial production should be robust for the month.

Despite some soft spots, the latest employment report is quite encouraging. The job gains will help pump up the recovery by supporting more consumer spending. For now, the employment gain is still not strong enough to bring unemployment down consistently. But increases in the 200,000 and higher vicinity in the near term should bolster a virtuous cycle of spending and hiring and eventually stronger payroll gains.

The consumer ended up with a fatter wallet in January but did not open it up as much as in recent months. Inflation remains on two tracks with headline numbers outpacing the core. Personal income in January increased 1.0 percent, following a 0.4 percent gain the month before. The latest figure was boosted largely by technical effects from last year’s payroll tax cuts. Wages & salaries, however, still grew a moderate 0.3 percent after gaining at the same pace in December. The consumer ended up with a fatter wallet in January but did not open it up as much as in recent months. Inflation remains on two tracks with headline numbers outpacing the core. Personal income in January increased 1.0 percent, following a 0.4 percent gain the month before. The latest figure was boosted largely by technical effects from last year’s payroll tax cuts. Wages & salaries, however, still grew a moderate 0.3 percent after gaining at the same pace in December.

As in December, consumer spending for the latest month was led by auto sales and higher gasoline prices. Personal consumption expenditures increased a modest 0.2 percent, following a 0.5 percent advance in December. For January, strength was led by nondurables, up 0.9 percent (including gasoline), with durables advancing 0.4 percent. Services spending was flat for the latest month. Unfortunately, inflation eroded the gain in overall spending as inflation-adjusted purchases fell 0.1 percent in January after a 0.3 percent boost the month before.

On the inflation front, the PCE price index posted a 0.3 percent rise, matching the gain in December. The core rate was not as strong but still warmed up a bit with a 0.1 percent rise, compared to no change in December. On a year-ago basis, headline PCE prices are up 1.2 percent in January-the same rate as in December. Core inflation held steady at 0.8 percent year-on-year versus in December. Of course, a big part of the sluggishness in the core rate is from weak housing cost inflation. On the inflation front, the PCE price index posted a 0.3 percent rise, matching the gain in December. The core rate was not as strong but still warmed up a bit with a 0.1 percent rise, compared to no change in December. On a year-ago basis, headline PCE prices are up 1.2 percent in January-the same rate as in December. Core inflation held steady at 0.8 percent year-on-year versus in December. Of course, a big part of the sluggishness in the core rate is from weak housing cost inflation.

Year on year, personal income for January was up 4.6 percent, compared to 3.8 percent in December. PCEs growth improved to 4.0 percent from 3.9 percent in December.

Income is up, which is good, but spending has slowed. For now, the easing in spending growth is not worrisome given that it is coming off strong months. However, moving forward, healthier gains in wages & salaries are going to be needed to keep spending ahead of what appears to be building headline inflation. The recent boost in payroll employment offers hope that personal income growth will be strengthening not far down the road.

The past recession led to deferred sales of motor vehicles and a rise in the age of the U.S. auto fleet. And now, consumers have decided it is time to trade in for something newer. Unit new sales of cars and light trucks jumped 6.4 percent in February. The total unit annual rate came in at 13.4 million, split evenly between growth for North American-made vehicles, to a 10.2 million rate, and growth for foreign-made vehicles, to a 3.2 million rate. But the split between cars and trucks is definitely not even, with gains concentrated clearly in cars in what is a visible reaction to high gas prices. The past recession led to deferred sales of motor vehicles and a rise in the age of the U.S. auto fleet. And now, consumers have decided it is time to trade in for something newer. Unit new sales of cars and light trucks jumped 6.4 percent in February. The total unit annual rate came in at 13.4 million, split evenly between growth for North American-made vehicles, to a 10.2 million rate, and growth for foreign-made vehicles, to a 3.2 million rate. But the split between cars and trucks is definitely not even, with gains concentrated clearly in cars in what is a visible reaction to high gas prices.

Looking ahead on the economic calendar, the motor vehicle sales will support a strong auto component in the upcoming retail sales report. Additionally, auto makers will be encouraged to maintain plans for boosting auto assembly rates.

According to the latest reading by the Institute for Supply Management, manufacturing is gaining momentum. The ISM composite index advanced 0.6 point to 61.4 in February. The latest is the highest level since the same reading for May 2004 and the peak ISM for the last expansion. According to the latest reading by the Institute for Supply Management, manufacturing is gaining momentum. The ISM composite index advanced 0.6 point to 61.4 in February. The latest is the highest level since the same reading for May 2004 and the peak ISM for the last expansion.

February’s improvement was led by the employment and production components. The employment index jumped 2.8 points to 64.5 while the production index also gained 2.8 points, reaching 66.3.

Looking ahead, the new orders index only edged up 0.2 points but remained at a high level of 68.0. This is comparable to a high growth rate in the government series for new orders.

Overall, the manufacturing sector has re-emerged as a center of the economic recovery.

The economy is gaining strength not just in manufacturing. The ISM non-manufacturing composite index firmed to 59.7 in February from 59.4 the prior month. The latest is the strongest reading since 61.3 seen for August 2005 and indicates that the bulk of the economy is accelerating. The economy is gaining strength not just in manufacturing. The ISM non-manufacturing composite index firmed to 59.7 in February from 59.4 the prior month. The latest is the strongest reading since 61.3 seen for August 2005 and indicates that the bulk of the economy is accelerating.

February's strength in the composite index is centered in the business activity component (akin to a production reading on the manufacturing side) and in employment which came in at 55.6 for a more than one point gain and the best reading of the recovery.

The ISM non-manufacturing index should be healthy in the near term as the new orders index remained quite elevated, posting at 64.4 (well above breakeven of 50) but nudging down a bit from 64.9 in January.

The housing sector—or at least the single-family component—appears to be sagging so far this year. The National Association of Realtor’s pending home sales index fell 2.8 percent in January to 88.9, indicating a month-to-month decline in used-home contracts and pointing to weakness for existing home sales in February and March. It generally takes one or two months for a contract to close. Year-on-year, the index is down 1.5 percent. The housing sector—or at least the single-family component—appears to be sagging so far this year. The National Association of Realtor’s pending home sales index fell 2.8 percent in January to 88.9, indicating a month-to-month decline in used-home contracts and pointing to weakness for existing home sales in February and March. It generally takes one or two months for a contract to close. Year-on-year, the index is down 1.5 percent.

The January breakdown shows declines in all regions except the largest, the South, which in the report's only good news rose 1.4 percent.

The recovery is gaining momentum in manufacturing, non-manufacturing, and the consumer sector. However, high oil prices threaten to dampen growth.

Will the favorable news for the consumer from the employment report carry over to other consumer indicators' First out is consumer credit on Monday. Jobless claims post on Thursday. At close of the week, the all important retail sales report prints as does consumer sentiment. Also, currency traders will be extra alert on Thursday with the release of the monthly international trade report.

Consumer credit outstanding in December rose $6.1 billion showing, for the first time in the recovery, gains for both revolving and non-revolving credit. Revolving credit, up $2.3 billion, rose for the first time in 27 months. Non-revolving credit, reflecting strength in vehicle sales, extended its run of strength with a gain of $3.8 billion. Looking ahead to January’s number, there may be some modest help from motor vehicle sales which edged up 0.6 percent for the month but the amount boosting consumer credit will depend in part on the share split of sales to consumers and to businesses.

Consumer credit Consensus Forecast for January 11: +$2.5 billion

Range: -$2.0 billion to +$5.0 billion

The U.S. international trade gap in December grew to $40.6 billion from an unrevised $38.3 billion deficit the prior month. By components, exports rose 1.8 percent, following a 1.0 percent gain in November. Imports jumped 2.6 percent after increasing 0.8 percent the month before. The widening of the trade deficit came from the petroleum gap which expanded to $25.3 billion from $20.1 billion in November. In contrast, the nonpetroleum goods differential shrank to $27.2 billion from $30.4 billion the month before.

International trade balance Consensus Forecast for January 11: -$41.0 billion

Range: -$42.2 billion to -$39.7 billion

Initial jobless claims fell a substantial 20,000 in the February 26 week on top of a 25,000 decline in the prior week. The number of claims, at 368,000, is the third sub 400,000 reading in the last four weeks. The four-week average, down 12,750 to 388,500, is the first sub 400,000 reading of the recovery. Importantly, the Labor Department reported no special factors clouding the data.

Jobless Claims Consensus Forecast for 3/5/11: 385,000

Range: 370,000 to 400,000

The U.S. Treasury monthly budget report showed a January deficit of $49.8 billion. Four months into the fiscal year the deficit is at $418.8 billion, down from $430.7 billion a year ago. Higher tax receipts are solid evidence of economic strength. Receipts are up 9.4 percent so far in the government's fiscal year with outlays up only 4.8 percent. Looking ahead, the month of February typically shows a deficit for the month. Over the past 10 years, the average deficit for the month of February has been $108.1 billion and $144.5 billion over the past 5 years. The February 2010 deficit came in at $220.9 billion.

Treasury Statement Consensus Forecast for February 11: -$225.0 billion

Range: -$240.5 billion to -$190.0 billion.

Retail sales in January posted a moderate gain of 0.3 percent, following a 0.5 percent boost in December. Excluding autos, sales printed at a 0.3 percent improvement, matching the increase the month before. A large gain in gasoline station sales boosted the ex autos figure. Sales excluding autos and gasoline rose only 0.2 percent after a 0.1 percent boost in December and a 0.4 percent advance in November. Looking ahead, sales should get some lift from higher gasoline prices and a jump in unit new motor vehicle sales which jumped a monthly 6.4 percent in February. However, severe winter weather in parts of the U.S. may have weighed on other components.

Retail sales Consensus Forecast for February 11: +1.0 percent

Range: +0.1 to +1.5 percent

Retail sales excluding motor vehicles Consensus Forecast for February 11: +0.7 percent

Range: +0.3 to +1.3 percent

The Reuter's/University of Michigan's Consumer sentiment index jumped sharply in February, rising to a much higher-than-expected 77.5, up 2.4 points from the mid-month reading and implying a very strong reading of nearly 80 for the last two weeks of the month. The latest reading is a three-year high. Strength the last two weeks has been centered in the leading component which is expectations. The assessment of current conditions showed little change from the mid-month reading. Higher gasoline prices may bump sentiment down a bit in the next reading.

Consumer sentiment Consensus Forecast for preliminary March 11: 76.5

Range: 74.8 to 80.0

Business inventories continued to build at a steady rate in December rising 0.8 percent for a year-on-year build of 8.0 percent. The stock-to-sales ratio was unchanged at 1.25. Looking ahead, factory inventories will give substantial lift to January’s overall figure. Manufacturers’ inventories jumped 1.3 percent for the month.

Business inventories Consensus Forecast for January 11: +0.8 percent

Range: +0.6 to +0.9 percent

R. Mark Rogers is the author of The Complete Idiot’s Guide to Economic Indicators, Penguin Books, 2009.

Econoday Senior Writer Mark Pender contributed to this article.

|